Futures Rebound As Markets Celebrate TACO Tuesday

US equity futures rise as Trump leaves the door open for more discussions despite the 14 tariff letters sent yesterday and the extension of the deadline to Aug 1 which is „not 100% firm.” As of 8:15am ET, S&P futures rise 0.1% and Nasdaq futures gain 0.2% after US markets retreated on Monday from ATH on the back of increased tariffs on countries if deals are not reached (Japan/South Korea’s 25% were standouts). Pre-market, Mag7 names are all higher, while industrials are leading cyclicals with financials mixed. 10Y TSY yields are higher by 3bps to 4.41% as the curve bear steepens and the USD is higher after erasing an earlier loss. Commodities are generally weaker although Brent crude has once again rebounded from session lows to trade just shy of $70/bbl. The macro data focus today is on Small Biz Optimism (prints in line with expectations), 1-year Inflation Expectations, and an update on Consumer Credit.

In premarket trading, Magnificent Seven stocks are all higher (Tesla +1%, Nvidia +0.7%, Meta +0.5%, Amazon +0.3%, Alphabet +0.4%, Microsoft is little changed, Apple +0.06%).

- Clean energy stocks including Enphase Energy (ENPH) and SolarEdge (SEDG) fall after President Donald Trump called for new rules that would restrict access to tax incentives for solar and wind projects that were already pared back in his $3.4 trillion budget bill. Enphase Energy -2.9%, SolarEdge -6%

- Capital One Financial Corp. (COF) rises about 1% after TD Cowen analyst Moshe Orenbuch raised the recommendation on the credit-card issuer to buy from hold, seeing upside after its purchase of Discover and the potential for significant buybacks in the future.

- Ciena (CIEN) falls 3% as Morgan Stanley cuts to underweight, citing a lack of margin upside in the near term.

- Circle Internet (CRCL) slips about 2% after the stablecoin issuer was initiated with a second sell-equivalent rating, this time at Mizuho, with the bank seeing a 25% to 30% potential downside to consensus revenue for 2027.

- Datadog (DDOG) falls 2.5% as Guggenheim Securities cut to sell from neutral citing to near-term OpenAI optimization risk.

- Merit Medical Systems Inc. (MMSI) rises 2% after the the catheter maker reported preliminary 2Q revenue that topped estimates and named a veteran of Medtronic as its next CEO.

- UWM Holdings (UWMC) is up 2.3% after an upgrade to overweight from equal-weight by Barclays, which says the stock looks discounted enough to step in.

For stock markets, TACO Tuesday’s calm reflected traders’ belief in a familiar pattern of US President Donald Trump escalating his trade war only to later de-escalate. In the latest round, Trump said he was still open to negotiations and postponed duties of 25% or more on a list for trading partners until at least Aug. 1.

“Equity markets are focused on the positive news,” said Wolf von Rotberg, equity strategist at Bank J. Safra Sarasin. “Europe is working toward securing a framework agreement with the US and the July 9th deadline was pushed out by another month. The market has learned to focus on the facts more than following the talk.”

Ongoing talks with the European Union are likely to draw particular attention. The bloc is seeking to finalize a preliminary agreement this week that would lock in a 10% tariff rate beyond Aug. 1 while a permanent deal is hammered out.

The prospect of a better-than-expected trade deal helped boost the euro. The common currency rose as much as 0.5%, extending gains for the year as traders reacted to a Politico report that said the US offered a deal that would keep the 10% baseline tariffs, with exemptions for sensitive sectors.

“The fact that higher tariffs have become the default if no deal is reached does introduce a layer of risk that markets will have to price in,” said Daniela Sabin Hathorn, senior market analyst at Capital.com. “The dollar could struggle as this would have a negative impact on the growth outlook in the US.”

So far, the US economy has held up under the threat of a spiraling global trade war. Hiring is healthy, while the S&P 500 hit an all-time high last week. Still, some investors remain cautious that persistent policy uncertainty, along with concerns over rising levels of government debt and geopolitical headwinds, could eventually catch up with markets.

“Investors betting on the TACO trade might gradually face some disappointment,” said Raphael Thuin, head of capital markets strategies at Tikehau Capital in Paris. “There’s a real possibility that tariffs are here to stay beyond Trump’s mandate as a permanent fiscal tool to fund growing deficits.”

European stocks are in a narrow range, with Stoxx 600 fluctuating between gains and losses as European Union negotiators rushed to conclude a preliminary trade deal with the US to avoid a spike in tariffs, with miners, financial services and travel stocks outperforming, while real estate shares lag. Drinkmakers gain on tariff news, while renewables drop as the Trump administration targets tax breaks. Germany’s DAX marginally outperforms. Here are the most notable European movers:

- Kinnevik gains as much as 6.1% after the Swedish investment group reported its latest earnings. Degroof says the results were “slightly better than expected,” with net asset values above the broker’s estimates

- Zealand Pharma shares rise as much as 3.5%, among the top performers in the Stoxx 600 Health Care Index on Tuesday, after Barclays initiated coverage on the stock with an overweight recommendation

- Shares of drinksmakers rise after reports saying the European Union is seeking an exemption from the US tariff for certain products; Remy Cointreau gains as much as 4.2%, Pernod Ricard +3.6%, Campari +2.7%

- Glencore shares rise as much as 2.1% after JPMorgan resumed its coverage with an overweight recommendation, citing value-accretive strategic optionality and a potential coal de-merger

- NTG Nordic Transport Group rises as much as 4.7% after being awarded a new overweight rating from Barclays, with analysts arguing the stock is inexpensive and has significant potential upside

- Renewables stocks fall in Europe as President Donald Trump called for new rules that would restrict access to tax incentives for solar and wind projects that were already pared back in his $3.4 trillion budget bill

- Dr Martens and Pandora are among stocks underperforming in Europe after President Trump outlined plans to impose tariffs on goods from key supplier countries including Indonesia, Thailand and Cambodia

- TGS shares drop as much as 12%, the most since April, after the Norwegian geophysical services company reported preliminary second-quarter results. The company noted “challenging operational conditions”

- Betsson shares drop as much as 6.1%, the most in three months, after DNB Carnegie downgrades the stock to hold from buy. Analysts note that the online gaming firm is set for a period of slower revenue growth

- Victrex shares slump as much as 15% to the lowest since August 2009 as the polymer supplier’s trading update disappoints analysts, who see scope for double-digit cuts to full-year pretax expectations

- AB Dynamics shares drop as much as 1.2% after the company announced that CEO James Routh is leaving the business to take up the same role at fellow London-listed Victrex

- BNP Paribas Bank Polska drops as much as 5.1% after the European Bank for Reconstruction & Development sold 2.35m shares via accelerated book-building at discount to Monday’s closing price

Earlier in the session, stocks in Asia advanced as investors shrugged off US President Donald Trump’s tariff announcements and focused on room for further negotiations. The MSCI Asia Pacific Index gained 0.4%, with SK Hynix and Hitachi providing the biggest lift while BHP Group and Nintendo weighed on performance. South Korea and Japan both advanced on cautious hopes that the countries can reach trade deals ahead of Trump’s newly-extended tariff deadline. Trump earlier sent letters to Tokyo and Seoul, threatening levies of 25% beginning Aug. 1. Elsewhere in the region, Hong Kong shares rose, helped by a rebound in e-commerce giants Meituan and Alibaba. Their shares had been falling recently due to concerns over an intensifying price war in the food delivery business.

In FX, we initially saw broad dollar weakness after President Trump suggested he’s open to more negotiations on tariffs beyond an August 1 deadline, but that weakness has since reversed and the dollar is trading near yesterday’s highs. Aussie dollar tops G-10 peers after the RBA surprise. The yen underperforms.

In rates, bonds sell off across Europe and the US, taking their cue from jitters in Japan over the country’s political situation and associated fiscal risks. Japanese 30-year bond yields rose as much as 13 basis points. Australian bonds also slump after the RBA unexpectedly kept interest rates unchanged. That fed into weakness in the long-end across Europe. 30-year bund yields hit the highest level since March, benchmark 10-year yields up by around five basis points across countries. A flurry of supply is also weighing. 10-year Treasury yields up three basis points to 4.415%, at session highs with German and UK counterparts cheaper by an additional 2bp. Treasury auction cycle begins with $58 billion 3-year new issue at 1pm New York time, followed by $39 billion 10-year and $22 billion 30-year reopenings Wednesday and Thursday. WI 3-year yield near 3.875% is about 10bp richer than last month’s, which tailed by 0.4bp.

In commodities, gold is down by $12 to around $3,324/oz. Oil prices lower, Brent drops 0.7% to just over $69/barrel.

Looking at today’s calendar, US economic data slate includes June NY Fed 1-year inflation expectations (11am) and May consumer credit (3pm). The Fed speaker slate blank, with minutes of June FOMC meeting are to be released at 2pm tomorrow.

Market Snapshot

- S&P 500 mini +0.1%

- Nasdaq 100 mini +0.3%

- Russell 2000 mini +0.3%

- Stoxx Europe 600 little changed

- DAX +0.2%, CAC 40 little changed

- 10-year Treasury yield +3 basis points at 4.41%

- VIX -0.5 points at 17.28

- Bloomberg Dollar Index -0.2% at 1194.53

- euro +0.4% at $1.175

- WTI crude -0.7% at $67.45/barrel

Top Overnight News

- Following Trump announcing 25% tariffs on good from Japan starting Aug 1, Japan and the US are “actively” continuing negotiations. A Top trade negotiator from Japan said Japan’s trade deal with the U.S. must include tariff concessions for its vital automobile industry. RTRS

- Trump said Monday the U.S. would resume providing Ukraine with arms to help it withstand Russian attacks after months of trying without success to draw Moscow into negotiations on ending the war. WSJ

- President Trump on Monday indicated there may be some wiggle room for nations to negotiate on trade despite his fresh threat of additional tariffs going into effect on Aug. 1. When asked, he said “No, I would say firm, but not 100 percent firm. If they call up and they say ‘we’d like to do something a different way,’ we’re going to be open to that. But essentially that’s the way it is right now.” The Hill

- Apple’s top AI models executive Ruoming Pang is leaving for Meta’s new superintelligence group, people familiar said, marking another setback in the iPhone maker’s struggling AI efforts. BBG

- Kevin Warsh, one of the lead candidates to replace Powell as Fed chief, said rates should be lower and doesn’t think tariffs will fuel inflation. BBG

- China has strongly criticized companies and local governments for fuelling overproduction that it blames for driving down prices, as inflation figures this week are expected to show that one of the country’s longest bouts of factory price deflation is running unchecked. FT

- China warned the Trump administration on Tuesday against reigniting trade tension by restoring tariffs on its goods next month, and threatened to retaliate against nations that strike deals with the United States to cut China out of supply chains. RTRS

- Europe’s largest port is gearing up for a potential conflict with Russia by reserving space for ships carrying military supplies and planning where to divert cargo if war breaks out. FT

- Samsung’s profit more than halved on inventory writedowns following US curbs on Chinese-bound AI chips. BBG

- China’s CPCA says Tesla exported 10,115 Chinese-made vehicles in June (May 23,074)

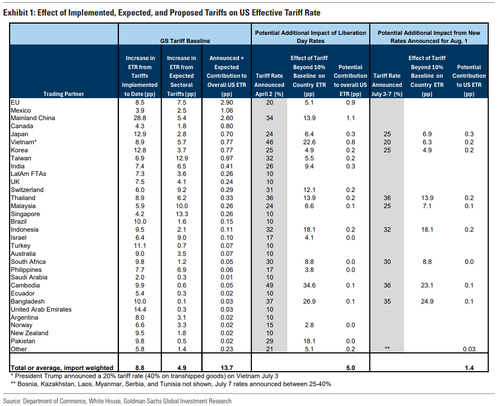

Trade/Tariffs

- US President Trump said regarding tariffs that the August 1st deadline is firm but he is open to other ideas, while Trump said he is close to making a trade deal with India and may adjust tariffs for some countries.

- White House announced that President Trump signed an executive order extending the tariff deadline to August 1st.

- US reportedly offered the EU a 10% tariff deal with caveats, although negotiations are still fluid, with any trade agreement subject to final approval by US President Trump, according to POLITICO.

- EU Commission President von der Leyen said Europe must show strength in trade negotiations with the US. Thereafter, German Finance Minister says if the EU does not reach a „fair” deal with he US, the bloc is ready to take counter-measures.

- Japanese PM Ishiba said haven’t been able to reach an agreement because Japan kept defending what needs to be defended, and will continue dialogue with the US and seek a chance of agreeing on a deal that benefits both countries. Ishiba added they were able to avert a hike in tariffs to 30%-35%, as result of past negotiations, and the US has proposed to continue talks until the new August 1st deadline.

- Japanese Finance Minister Kato said they expect the US stance to change as they continue trade negotiations, while they will take necessary steps to help industries cope with US tariffs while communicating with other agencies.

- Japanese Tariff Negotiator Akazawa held a call with US Commerce Secretary Lutnick. Agreed to actively engage in trade negotiations. Auto sector is core to Japan’s economy, can not tolerate the fact 25% tariffs on autos, and the auto parts tariff is inflicting huge losses on Japanese firms. No point in striking a US deal without an autos agreement.

- South Korea will step up trade negotiations with the US to win mutually beneficial results and clear up uncertainties caused by tariffs, while it added that trade talks with the US will be a chance to advance both countries’ key industries through the 'Renaissance Partnership’.

- The UK is set to miss the original deadline to close its steel/aluminium trade deal with the US, according to Sky’s Conway; Insiders say still some way from a breakthrough. However, „they are hopeful Donald Trump won’t raise UK tariffs from 25% to 50% for the time being, despite having promised to on July 9th”.

- Indian refiners reportedly plan to source around 10% of LPG imports from the US in 2026 in an attempt to reach a trade deal, according to Reuters sources.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly traded with cautious gains as participants digested the latest trade-related developments including US President Trump’s tariff letters to 14 countries so far including Japan, South Korea, South Africa, and Thailand with tariff rates ranging between 25%-40% and warnings against retaliation, although he also signed an Executive Order to delay the tariff deadline to August 1st. ASX 200 was indecisive as strength in tech and gold producers offset the losses in defensives, while an improvement in NAB Business Confidence was met with little fanfare as participants awaited the RBA rate decision which ultimately disappointed as the central bank defied the broad consensus for the first back-to-back cut since the pandemic, and instead decided to pause on rates through a 6-3 majority vote. Nikkei 225 recouped initial losses as recent currency weakness helped investors shrug off the tariff-related news with Japan facing a 25% tariff which is slightly higher than the 24% rate announced on Liberation Day. Hang Seng and Shanghai Comp were underpinned with the PBoC to support more onshore investors to invest in offshore bonds, while it will also expand the Bond Connect to include Chinese brokers, funds, wealth managers and insurers.

Top Asian News

- PBoC said it will support more onshore investors to invest in offshore bonds and will expand the bond connect to include Chinese brokers, funds, wealth managers and insurers, while it will also increase the quota under the swap connect.

- Chinese President Xi stressed developing the real economy to build up national strength and said the real economy should not be abandoned, nor should the traditional industries, according to Xinhua.

- Chinese Premier Li Qiang said China is confident in driving economic growth and has the resources to counter external headwinds.

- RBA unexpectedly kept the Cash Rate unchanged at 3.85% (exp. 25bps cut) with the decision made by a majority of 6-3 votes, while it stated that the Board will be attentive to the data and evolving assessment of risks to guide its decisions. RBA also noted that inflation has continued to moderate and the outlook remains uncertain although the Board continues to judge that the risks to inflation have become more balanced and the labour market remains strong. Furthermore, the Board remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply and it judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5% on a sustainable basis.

- RBA Governor Bullock says there will be more data and news by the next meeting. Made good progress on inflation, been within the target range for only one quarter thus far. Effect of 50bps of cuts is still to flow through. CPI interpretation was different to the markets, decision was about timing rather than direction; monthly CPI is too volatile, the quarterly figure could be higher. Confident they are on a path to ease further. On an easing path, timing is the question. Was an active debate within the RBA boardroom, the difference between the sides was not about direction. Bullock will not say how she voted.

European bourses opened higher, welcoming Trump’s confirmation that the new tariff deadline is August 1st and as Monday’s letters did not have any narrative-shifting surprises. Since, benchmarks have come off best and are either side of the unchanged mark, Euro Stoxx 50 U/C. Sectors in-fitting with the above and as such are now mixed. Basic Resources lead amid gains in Glencore (+2.5%) after an upgrade by and favourable commentary from JPMorgan. Retail at the other end, hit by the tariff letters on Asian manufacturing nations which are a key destination for European names such as Pandora (-1.1%).

Top European News

- German Finance Minister Klingbeil says they see that economic sentiment has improved.

- UK OBR says „public finances in relatively vulnerable position and facing mounting risks”, adds UK debt set to exceed 270% of GDP by early 2070s.

FX

- USD has been giving back some of Monday’s gains, upside that occurred alongside an increase in angst into the tariff letters. Ultimately, the main takeaway was Trump providing more time for negotiation and as such the TACO trade remains in play. DXY is currently tucked within yesterday’s 96.89-97.66 range, currently just off highs of 97.43.

- AUD outperforms as the RBA surprisingly kept rates unchanged in a 6-3 vote, despite markets pricing in a 95% chance of a move pre-release. AUD/USD back above 0.65 but yet to breach Monday’s 0.6564 peak.

- Upside that has pulled the Kwi along with it, NZD/USD has made its way back onto a 0.60 handle but is still some way off yesterday’s 0.6063 high (current session peak @ 0.6034).

- EUR the next best, benefitting from reports which suggest 10% baseline tariffs remain an option for the EU. EUR/USD is currently firmer, just off a 1.1765 peak within Monday’s 1.1686-1.1790 range.

- GBP just about in the green against the USD, but Cable is back to its earlier 1.36 base. A bout of further pressure emerged on an OBR risk report which laid out that „public finances in relatively vulnerable position and facing mounting risks”, adds UK debt set to exceed 270% of GDP by early 2070s

- PBoC set USD/CNY mid-point at 7.1534 vs exp. 7.1772 (Prev. 7.1506)

Fixed Income

- Complex pushed lower by the tariff deadline extension and a packed supply docket.

- USTs saw a slightly softer start to the day, given the constructive risk tone. Similar story for EGBs and Gilts, though the magnitude of downside has increased throughout the morning, USTs to a 110-25+ trough, taking out Monday’s 110-29 base and now teetering just above 110-25, the WTD low from the last week of June.

- EGBs also dented, but with losses much more pronounced. Bunds lower by near 50 ticks. As referenced, pressure in EGBs has been increasing, an intensification that began alongside the constructive European cash equity open; furthermore, supply is weighing and the passing of some taps e.g. Germany failed to provide any relief (unsurprising, the German auction was somewhat soft and we await details on EU supply).

- For the most part, an absence of specifics for the UK. No follow through in Gilts from the OBR reporting that domestic finances are in a „relatively vulnerable position and face mounting risks”. Nonetheless, Gilts lag with downside intensifying and the benchmark now looking to lows from mid-June, incl. 91.16.

- Germany sells EUR 3.754bln vs exp. EUR 5bln 2.20% 2030 Bobl: b/c 1.50x, average yield 2.26% & retention 24.92%.

Commodities

- Crude benchmarks are lacklustre, largely unaffected by trade updates with volumes light and awaiting further geopolitical updates from the Middle-East; Brent trades within a narrow USD 69.03 to 69.61/bbl range, re-approaching overnight lows following news regarding the resumption of Israel-Hamas Doha talks.

- Precious metals softer, dented by the broadly constructive risk tone in-fitting with pressure seen in other traditional havens (i.e. fixed and JPY). Though, downside is limited thus far with the softer USD and general tariff uncertainty, despite the welcome confirmation of an August 1st deadline, preventing a more concerted move lower. XAU down to a USD 3324/oz base and within Monday’s USD 3296-3343/oz band.

- Base metals, in contrast, welcome Trump signing an executive order pushing the tariff deadline to August 1st (prev. July 9th) and as the first batch of tariff letters didn’t contain anything particularly shocking. 3M LME Copper holds at the upper-end of a USD 9793-9889 band. However, it remains shy of Monday’s USD 9871 peak and last week’s USD 9889 best.

- US President Trump signed an Executive Order aiming to end subsidies for foreign-controlled energy sources.

Geopolitics

- US President Trump said he’s got great cooperation from countries neighbouring Israel, when asked about Palestinian relocation plans. Trump noted Iran talks are scheduled and that Iran will not be a nuclear state, while he hopes they don’t have to do another strike on Iran.

- White House said US Envoy Witkoff is to travel to Doha later this week for a Gaza ceasefire, while it was separately reported that Witkoff said they have an opportunity to get a peace deal in Gaza and that the Iran meeting will be in the next week or so.

- Subsequently, Iran’s MFA Spokesman told state TV: „We have not handed in any requests to meet with the Americans”, via France24.

- UKMTO says a vessel sustained significant damage and lost all propulsion after being attacked by 5 rocket grenades, 51NM West of Yemen’s Hodeidah; vessel is under continuous attack and authorities are investigating.

- Ceasefire talks with Gaza have recommenced, in Doha, via journalist Elster (08:49BST/03:49ET).

- US President Trump said they have to send more weapons to Ukraine and that they have to defend themselves, while the Pentagon later announced the Department of Defense will send additional defensive weapons to Ukraine.

- German Foreign Ministry says the Chinese Military has used a laser to target a German aircraft in EU operation aspides; Chinese ambassador summoned,

US Event Calendar

- 6:00 am: Jun NFIB Small Business Optimism, est. 98.6, prior 98.8

- 3:00 pm: May Consumer Credit, est. 10.55b, prior 17.87b

DB’s Jim Reid concludes the overnight wrap

A quiet day where we were all waiting for tariff news sprung into life just after Europe closed yesterday as the first major tariff news of the week broke. In a series of posts on social media, President Trump announced new tariff rates on several trading partners. He started off by announcing 25% tariff rates against Japan and South Korea, effective August 1st. This was followed by “trade letters” to a further twelve countries including South Africa (30% rate), Malaysia (25%), and Indonesia (32%). President Trump also said that “any goods transshipped to evade a higher tariff will be subject to that higher tariff,” while noting that these would be separate from the sectoral tariffs. The headline rates for most countries announced yesterday were around the same levels as the Liberation Day tariffs, but President Trump also said that if countries were to raise their tariffs in response, then “whatever number” they choose will be added onto the 25% charged by the US.

White House Press Secretary Leavitt announced that more letters will be arriving throughout the week. After sending the posts, the President signed an executive order that effectively delays the new tariff rates until August 1, prolonging the current 10% tariff rate and giving nations more time to meet the trade demands from the White House. The President continued to signal he was open to deals, saying the August 1st deadline was “not 100% firm” and that they could “maybe adjust a little bit, depending.” Overnight, Politico reported that while a US-EU trade deal had not been finalised, the US had offered the EU a 10% tariff rate with caveats. Given the higher rates seen earlier in the day for other trading partners, the EUR has rallied (+0.32%) overnight and is back to levels before the letters started rolling out yesterday.

Stocks fell in response to the tariff news, although the S&P 500, which closed -0.79%, was already -0.6% just before the announcement in anticipation of the noon Washington timeline that had been given over the weekend with regards to letters being sent out. The index was down -1.25% at the lows of the day, before rebounding as investors priced in the possibility of trade deals getting over the line for larger trading partners before putative tariffs kick in.

Within US equity markets, the Magnificent 7 (-1.03%) underperformed while following a similar pattern to the broad index, although the index was also weighed down by Tesla (-6.79%), which saw the biggest decline in the entire S&P after Musk announced the formation of the “America Party” over the weekend. Small caps, which have less margin to absorb tariff costs, underperformed by even more as the Russell 2000 fell by -1.55%. Meanwhile, US Treasuries also struggled, with the 10yr yield up +3.4bps to 4.379%, whilst the 30yr yield (+5.4bps) rose to 4.92%. In turn, that helped to support the US Dollar index (+0.31%), which has stabilised around a 3-year low in the last week.

President Trump posted late on Sunday that any country aligning with the “Anti-American policies” of the BRICS would face an added 10% tariff, and this didn’t help the likes of Brazil’s IBOVESPA (-1.26%). The 10 member states met in Rio Janeiro over the weekend, where they condemned US and Israeli strikes on Iran, as well as the US unilateral tariffs. So, yet another tariff threat that adds to the uncertainty.

In the meantime, one ongoing theme was the continued pressure on the Fed from the administration. That came as Peter Navarro wrote in a Substack post that Chair Powell’s policy was causing American households “acute financial pain” and that if Powell “will not voluntarily adjust course, the board must act decisively to prevent further economic harm.” We’ll get the June FOMC meeting minutes release tomorrow, so that should offer more details on how officials are thinking about rate cuts. At face value, the latest tariff letters, and the fact that the deadlines seem to be pushing towards August 1st, thus prolonging uncertainty, means a September Fed cut will become more difficult unless there is strong evidence of a deteriorating economy.

Over in Europe, equities had put in a more positive performance, but closed before the stream of tariff headlines came through. Sentiment was also boosted, however, by hopes of a trade deal, with EU spokespeople earlier confirming to Bloomberg that they were close to a trade agreement with the US, after a “good exchange” between Von Der Leyen and President Trump. So that meant the STOXX 600 (+0.44%) and the DAX (+1.20%) both advanced. European futures are only lower by around a couple of tenths this morning. Away from the EU, the FTSE 100 (-0.19%) lagged behind yesterday. European sovereign bonds traded more in line with US Treasuries, with yields on 10yr bunds (+3.6bps), OATs (+4.2bps) and BTPs (+4.7bps) all moving higher. We also found out German industrial production rose +1.2% in May (vs. -0.2% expected), which was relatively stronger than the French and Spanish numbers last week.

Asian equity markets are higher this morning shrugging off the threats of increased US trade tariffs as President Trump left the door open for additional trade negotiations. Across the region, the KOSPI (+1.46%) is leading gains while the Hang Seng (+0.86%), the CSI (+0.74%), the Shanghai Composite (+0.58%) and the Nikkei (+0.28%) are also higher. The S&P/ASX 200 (-0.19%) is trading lower but has hardly had time to react to a surprise 6-3 decision, just before we go to print, to hold rates rather than cut them as widely expected. The RBA’s statement pointed to an „uncertain outlook” as the reason for holding rates. The Australian dollar reacted sharply, jumping to 0.6539 against the dollar, while policy-sensitive 3-year government bond yields have climbed 14bps, 10 of which have come in the last few minutes after the decision. Governor Michele Bullock’s upcoming press briefing is now the focus of market attention. Elsewhere US equity futures are flat to up a tenth of a percent.

On geopolitics, yesterday Iran announced that Israel had tried to assassinate its President during last month’s attacks, and that US strikes has severely damaged its nuclear infrastructure and equipment. In an interview with Tucker Carlson on Monday, Iran’s President Masoud Pezeshhkian said that the US could resolve its differences with Iran through dialogue and talks, but said it was difficult to trust the US and asked how they could be sure Israel wouldn’t be given permission to attack again. Amidst the newsflow, WTI rose +1.39% to $67.9/bbl and Brent crude was up +1.87% to $69.58/bbl even with the surprise oil production increases announced by OPEC+ over the weekend. It’s back down around half a percent this morning.

To the day ahead now, we’ll have the US June NFIB small business optimism, the NY Fed’s inflation expectations, and Germany’s trade balance for May. Central bank speakers include the ECB’s Nagel.

Tyler Durden

Tue, 07/08/2025 – 08:30